Finished reading? Continue your journey in Tech with these hand-picked guides and tutorials.

Boost your workflow with our browser-based tools

Share your expertise with our readers. TrueSolvers accepts in-depth, independently researched articles on technology, AI, and software development from qualified contributors.

TrueSolvers is an independent technology publisher with a professional editorial team. Every article is independently researched, sourced from primary documentation, and cross-checked before publication.

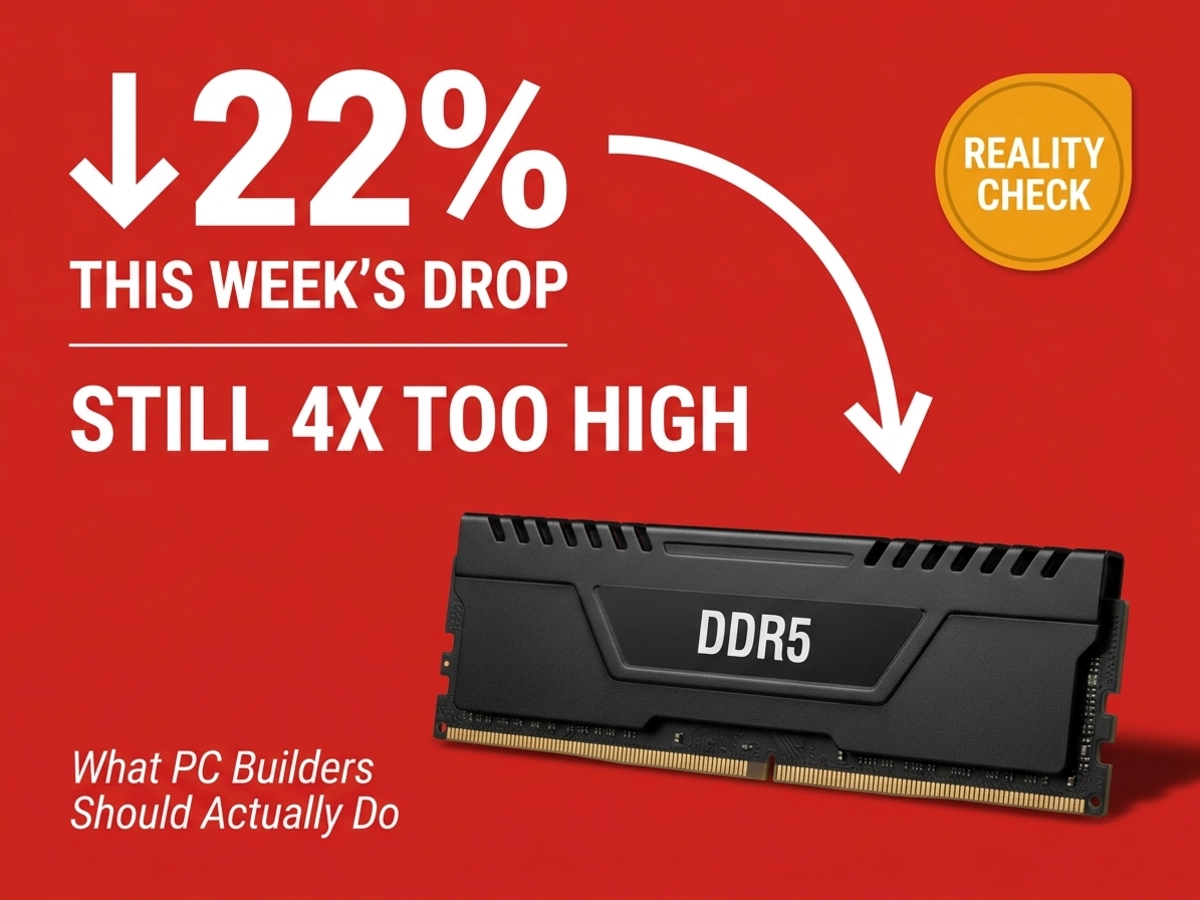

DDR5 prices fell up to 22% this week after Google's TurboQuant sent memory stocks into a panic. But those "deals" still sit 3.5 to 4 times above pre-crisis lows, and TurboQuant cannot touch the structural wafer shortage that put them there. Here's what the market got wrong, and what PC builders should actually do.

Something genuinely unusual happened in US retail memory markets at the end of March 2026: prices moved down. TrendForce's news coverage confirmed that Corsair's VENGEANCE 32GB DDR5-6400 kit fell to around $379.99 from a recent peak of $490, a decline of more than 20%, while 16GB modules dropped from $260 to $219.99. For a market that had been moving in one direction for months, any reversal looks like relief.

Our read of where that relief actually lands changes once you pull up the historical baseline. That same 32GB DDR5 kit was selling in the $100 to $200 range as recently as October 2025. A PC Gamer pricing investigation found that the Corsair Vengeance RGB DDR5-6000 32GB, which the outlet's author personally purchased for around $90 three years ago, sat at $370 after the TurboQuant dip. At Newegg, G.Skill's Trident Z5 32GB DDR5-6400 was still $500 after a promotional $50 reduction. Crucial's Pro OC 64GB kit remained at $630 following its discount. These are not bargains in any absolute sense.

The Corsair reduction also turns out to be more complicated than it appears. PC Gamer's direct pricing investigation found the Corsair Vengeance RGB DDR5-6000 had already dipped to $370 in early March, before Google published the TurboQuant research on March 24. The brand's relative affordability compared to competitors appears to be a pre-existing market positioning rather than a TurboQuant effect. Other manufacturers' prices show far smaller movements or continued upward pressure, and the discount landscape is concentrated in one vendor's product line rather than spread across the category.

The gap between "prices fell 20%" and "prices are now reasonable" is the entire story.

The KV cache, short for key-value cache, is the high-speed scratchpad a large language model maintains during inference. Every token a model generates gets stored there so the system does not have to recompute past context from scratch. As context windows grow longer, this cache grows proportionally, consuming increasing amounts of GPU memory and becoming a primary bottleneck for long-context AI deployment.

Google Research's TurboQuant blog post, published March 24, 2026 by research scientist Amir Zandieh and VP Vahab Mirrokni, reports that the algorithm compresses this cache to just 3 bits per value without requiring any model retraining or fine-tuning and with no measurable accuracy loss on tested benchmarks. At 4-bit precision, the paper reports up to an 8x increase in attention logit computation speed on Nvidia H100 GPUs compared to a 32-bit unquantized baseline. The paper is accepted as an ICLR 2026 poster and has not been accompanied by a deployment announcement or official code release.

The stock market heard "6x less memory" and sold first, asked questions later. CNBC reported that SK Hynix fell 6%, Samsung fell nearly 5%, and Kioxia dropped nearly 6% on the Korea Exchange on March 26, dragging the KOSPI index down 3.2%. Micron and SanDisk had already declined in US trading the prior session. Ben Barringer, head of technology research at Quilter Cheviot, told CNBC the selloff was largely profit-taking amplified by TurboQuant, characterizing the algorithm as "evolutionary, not revolutionary" and stating directly that it "does not alter the industry's long-term demand picture."

The gap between what TurboQuant compresses and what drives the DDR5 shortage is wider than we can overstate.

A 70-billion-parameter model running before and after TurboQuant requires exactly the same amount of high-bandwidth memory for its weights. The algorithm compresses only the inference-time scratchpad, not the library shelves.

Model weights — the stored parameters that define what a large model knows — are unaffected. Training workloads, where AI companies consume the most memory at the highest margins, are entirely untouched. The KV cache that TurboQuant compresses is the working memory of inference, not the foundational memory of the hardware procurement decisions that have been driving the shortage.

Micron's own earnings picture illustrates the disconnect between market sentiment and business fundamentals. After posting record quarterly revenue of $23.9 billion and guiding $33.5 billion for the next quarter, Micron's stock fell more than 20% from its post-earnings highs across six sessions, its steepest multi-session decline since April 2025. Micron's CFO Mark Murphy stated on the Q2 earnings call that "demand far exceeds supply" and confirmed that supply constraints would persist "beyond 2026." A compression algorithm targeting the inference KV cache does not change the calculus on that supply position.

The reason DDR5 prices quadrupled between mid-2025 and early 2026 has nothing to do with AI inference efficiency. It has everything to do with silicon wafer allocation. For a full account of why consumer DDR5 became so scarce so quickly, the structural forces at work stretch back well before TurboQuant entered the picture.

Each gigabyte of High Bandwidth Memory consumes roughly three times the wafer capacity of a gigabyte of standard DDR5. The three dominant memory manufacturers — Samsung, SK Hynix, and Micron — have been reallocating increasing shares of their advanced-process wafer capacity toward HBM because AI accelerator demand is larger, faster-growing, and significantly more profitable than consumer DRAM. According to available market data, up to 40% of advanced-process wafer capacity was committed to HBM production by the major manufacturers. IDC projected 2026 DRAM supply growth at only 16% year-on-year and NAND at 17%, well below historical norms while demand continued outpacing supply. The organization characterized the situation not as a cyclical imbalance but as a structural reallocation of global silicon wafer capacity.

The contract pricing data makes the retail dip look even more isolated. Tom's Hardware, citing TrendForce's latest memory pricing survey, projected Q2 2026 conventional DRAM contract prices to rise 58–63% quarter-over-quarter, with NAND Flash contract prices rising 70–75% QoQ. This follows a Q1 2026 in which DRAM contracts climbed 90–95% QoQ. These projections were issued independently of TurboQuant's announcement and reflect the underlying procurement reality that AI hyperscalers and cloud providers operate under long-term supply agreements. Retail sentiment dips do not move contract markets.

Hardware OEMs are pricing in an extended shortage with no ambiguity. MSI general manager Huang Jinqing told investors in March that the company planned to raise gaming hardware prices 15 to 30 percent over nine months in 2026, describing the year as "the most severe year since the company was founded." A 16GB DDR5 module that sold for approximately $40 about one year earlier had reached $170 to $180, with some spot transactions hitting $200. MSI was holding only one to two months of secure memory inventory and was actively pursuing multi-year supply contracts to reduce exposure.

We cannot confirm when contract pricing will reflect any downward pressure from TurboQuant, because no contract pricing data available as of April 2, 2026 shows that it has.

Samsung's Phase 4 Pyeongtaek expansion, SK Hynix's $8B ASML equipment order, and Micron's Idaho fab all share the same timeline: meaningful new supply arrives no earlier than 2027. New greenfield fabrication facilities require a minimum of three years from decision to volume production. The HBM allocations that created consumer DDR5 scarcity are locked into multi-year supply agreements with hyperscalers. TurboQuant operates at the software layer of inference stacks. The supply constraint operates at the silicon layer of fabrication plants. These are different systems, running on different timescales, and they do not interact.

The only compression breakthrough comparable to TurboQuant in recent memory is DeepSeek R1's inference efficiency gain in January 2025. It triggered the same selloff logic in Nvidia and memory stocks, and then validated the opposite outcome within two quarters. AI capital expenditure commitments from hyperscalers reached record highs in the months following the panic. The cheaper AI inference became, the more applications became viable, and the more hardware operators needed to serve them.

This pattern has a name in economics: the Jevons Paradox, first articulated by William Stanley Jevons in 1865, which observes that improvements in resource efficiency tend to increase rather than decrease total resource consumption. When the cost per unit of a capability falls, the number of viable applications for that capability expands, often by more than the efficiency savings reduce per-unit demand. In the AI context, TurboQuant lowers the inference cost per query. That makes long-context AI applications viable for organizations that previously found the cost prohibitive. Those organizations do not use less hardware than before; they begin using hardware they previously could not justify.

The Jevons Paradox is a compelling historical pattern, though we should note it is a probabilistic argument rather than a guarantee: past efficiency cycles and this one may not be identical.

The most direct evidence that the market overreacted is Google's own behavior. The TurboQuant paper was first posted to arXiv in April 2025; the March 2026 blog post was timed to coincide with the ICLR conference presentation, not a new research milestone. Despite having had access to its own compression research for nearly a year, Google raised its calendar year 2026 capital expenditure guidance to approximately $180 billion, up roughly 100% year-over-year. A company that genuinely believed its compression research would reduce hardware needs does not simultaneously double its hardware spending. Bank of America's Vivek Arya made the same point to clients, noting that comparable compression techniques have existed since 2024 without altering hardware procurement at scale.

Morgan Stanley put a sharper frame on TurboQuant's actual technical effect: the algorithm expands how much work a single GPU can do per memory dollar, enabling longer context windows and more concurrent user sessions from the same hardware budget. That is a cost efficiency improvement for AI operators. It is not a signal that memory procurement volumes will fall.

Buyers who need RAM today face a different calculus than buyers who can wait, and understanding that difference matters more than any judgment about TurboQuant itself. The current discounts on Corsair products are real compared to the March 2026 highs. Someone who needs 32GB of DDR5 today can find it for less than they would have paid three weeks ago — a meaningful near-term improvement even if it represents a fraction of what would be needed to return to pre-crisis pricing.

The available evidence suggests TurboQuant's production-level compression benefit is meaningful but likely smaller than the headline 6x figure implies for inference stacks already running quantized operations. The 6x benchmark is measured against 32-bit unquantized floating-point keys, which is not how most production AI inference runs. Real-world deployment benefits are genuine, but the figure that drove the stock selloff is a best-case measurement, not a typical-case outcome.

What we cannot tell buyers is when prices return to pre-crisis levels, because the structural supply data available as of April 2026 points to 2027 at the earliest.

Tom's Guide put the clearest timestamp on the situation, recommending buyers hold until August 2026, framing the current market as a pricing standoff in which retailers have demonstrated they can discount to clear stock, but manufacturers retain the option to cut production and reduce availability if prices fall too far. That is the "phantom pricing" scenario: MSRPs improve on paper while actual stock availability keeps effective costs elevated.

Buyers who need RAM immediately for a build they cannot delay are in a better position than they were three weeks ago, and the Corsair deals specifically represent the best value per gigabyte in the current market. Acting on those discounts is reasonable if the need is genuine.

Buyers who can wait should wait. The structural supply constraint has not changed. Contract prices are projected to rise further in Q2 2026. Hardware manufacturers are raising prices across their product lines. The factors that created the shortage are still in place, and TurboQuant — a research paper without official code or a production deployment timeline — has not removed any of them. If the Jevons Paradox holds, AI efficiency gains will expand deployment and increase total memory demand over time rather than reduce it. If it does not, the supply constraint will still dominate the market through 2026.

Either way, the thesis that a KV cache compression algorithm resolves a silicon wafer allocation crisis was always the wrong question. The DDR5 price drop this week reflects market sentiment, not market fundamentals. The fundamentals haven't moved.